Board composition continues to be a primary area of focus, particularly as it relates to diversity and gender, in addition to tenure, overboarding and director skills.

Canadian reporting issuers have now completed five years following changes adopted by the Canadian Securities Administrators (CSA) to National Instrument 58-101 Disclosure of Corporate Governance Practices (NI 58-101) and Form 58-101F1 Corporate Governance Disclosure that, among other things, require the disclosure of certain information relating to the representation of women on boards of directors and in executive officer positions.

Diversity disclosure in respect of ‘designated groups’ beyond gender is generally required for Canada Business Corporations Act (CBCA)-incorporated public companies with the recent amendments to the CBCA.

In contrast to NI 58-101, venture issuers are not exempt from the CBCA diversity disclosure requirements that extend to four designated groups as defined under the Employment Equity Act, namely: women, indigenous people (First Nations, Inuit and Metis), persons with disabilities and members of visible minorities. The requirements apply to proxy circular disclosure regarding the board and senior management.

Board tenure and refreshment consider retirement age, term limits and broadening board skillsets to account for broader areas of risk and expertise.

NI 58-101 and the new CBCA diversity disclosure provisions require disclosure of director tenure limits and although there are not prescribed limits, there is growing guidance on what some consider to be lengthy tenure. Earlier this year, ISS published an expanded version of its Governance QualityScore, which identified lengthy director tenure as nine years. Compare this with the average tenure limit of Canadian issuers of 13 years, as reported in a CSA study last October that reviewed the annual disclosure of 641 Toronto Stock Exchange (TSX) issuers.

Developments in overboarding and interlocking are also areas to watch, particularly given their impact on this past year’s US director elections. Overboarding refers to when a director is on an excessively high number of public company boards, while cross-directorships refers to when two or more directors are also fellow directors of another public company.

According to the ISS QualityScore, a five-board maximum emerged as the new standard in 2019 for non-executive directors and a two-board maximum for the CEO, in addition to sitting on the board of the company where he or she is a CEO, for a total of three boards.

Other key findings of the 2019 CSA study are:

- 73 percent of issuers have at least one female director, up from 66 percent in 2018

- 33 percent of issuer board vacancies were filled by women, up from 29 percent in 2018

- 50 percent of issuers have adopted policies relating to female representation, up from 42 percent in 2018

- 5 percent of issuers have a female board chair, a new metric in 2019

- 21 percent of issuers have adopted term limits, which is consistent with 2017 and 2018.

OUR ANALYSIS OF THE S&P/TSX 60

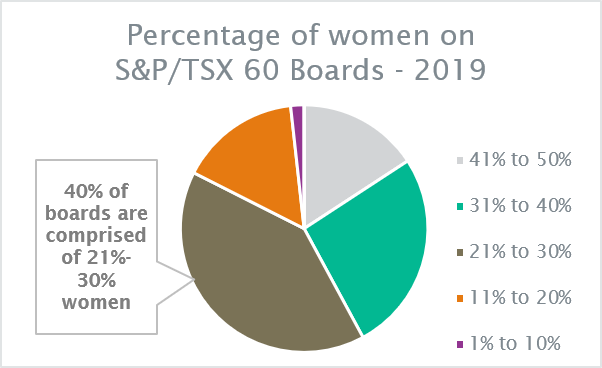

In our 2019 analysis of the annual proxy circular disclosure of the S&P/TSX 60, we took a closer look at diversity and tenure trends. We find that a plurality of issuers in this group (40 percent) have between 21 percent and 30 percent representation by women on their board.

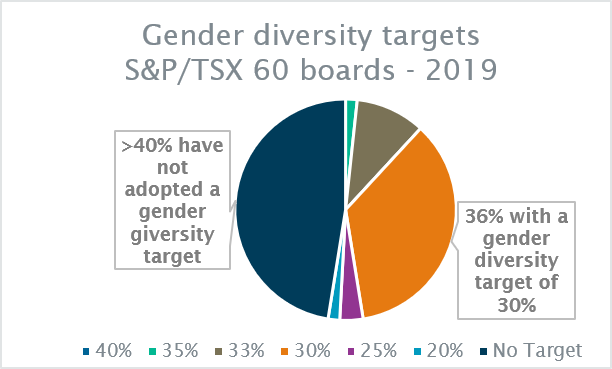

In terms of setting gender diversity targets for board composition, we find that 47 percent of issuers have no reported target, compared with 36 percent having a target of 30 percent women board members.

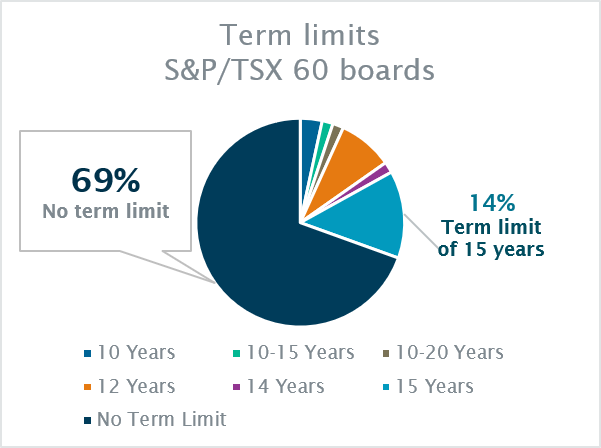

For term limits, we find that although most issuers do not impose term limits, 14 percent have set term limits of 15 years, as reported in 2019.

THE TAKEAWAY

Beyond awareness, we encourage you to consider what these trends and developments mean for your organization, specifically how they impact your annual meeting preparation and continuing corporate governance matters.

For many issuers, this means a strategic review of stakeholder-focused communication, including continuous disclosure materials as well as board and committee charters, company policies and underlying frameworks to consider whether updates are needed in areas such as the following:

- Identifying gaps in current disclosure, policies and materials, and determining options for your organization to address

- Reviewing the frameworks and processes that support disclosure, charters and policies, particularly as they relate to risk management

- Simplifying disclosure to focus on quality of disclosure specific to the organization, its business and its risks

- Aligning policies and/or public filings with regulatory and best practice updates and changes, while taking a fresh look to eliminate redundancies or inconsistencies.

Lisa Culbert is counsel for legal design & operations and Ramandeep Grewal is a partner with Stikeman Elliott in Toronto